Porque os impérios não caem com guerras...

Publicado em 25-03-2026

Quando a matemática se torna

irreversível e a história reluz…

Porque os impérios não caem com

guerras...

(for English, please scroll down)

A crise de Suez de 1956 foi um momento-chave

em que se tornou óbvio, para Londres e para o mundo, que o poder imperial

britânico e a centralidade da libra já não conseguiam sobreviver sem o aval

financeiro e político de Washington. Os paralelos com a situação actual do

dólar e dos EUA existem (pressão geopolítica, dívida elevada, contestação de

rivais), mas o ponto de partida é muito diferente: em 1956 o Reino Unido já

estava em declínio estrutural, enquanto os EUA continuam a ser, de longe, a

maior economia e o principal emissor de activos seguros, mesmo sob fogo de

processos de “desdolarização”.

A crise de Suez marca o início da

derrocada da libra e do declínio do Reino Unido. Em primeiro lugar, assinala

uma manifesta dependência dos dólares e a vulnerabilidade da libra. Após

a Segunda Guerra, a libra manteve um papel de moeda de reserva da “sterling

area”, mas foi apoiada por linhas de apoio americanas e pelo sistema de Bretton

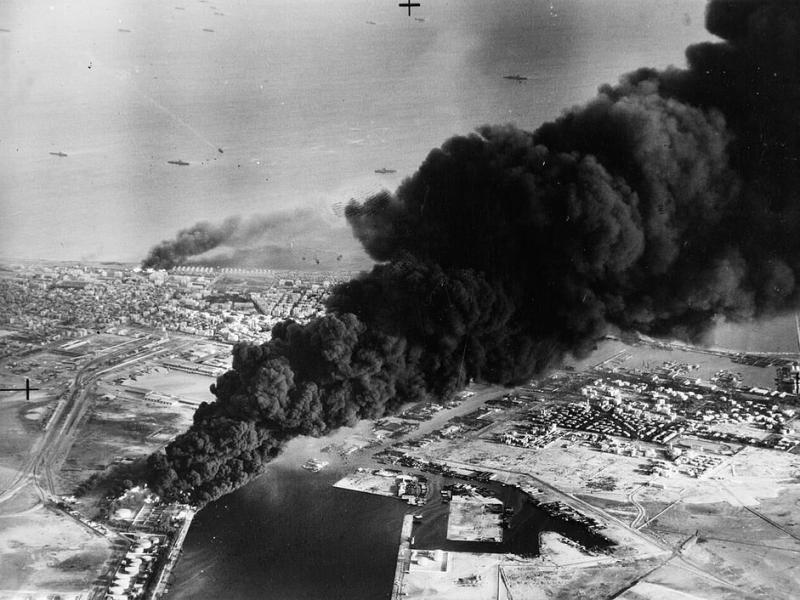

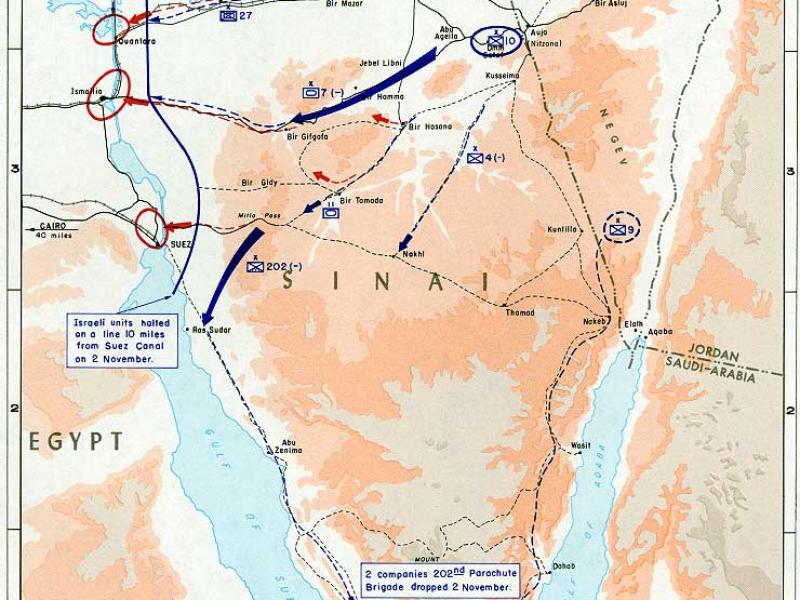

Woods (paridade fixa de 2,80 USD/GBP). A nacionalização do canal de Suez pelo

presidente egípcio Nasser (1918-1970, presidente 1954-1970), em Julho de 1956,

e a intervenção militar anglo-franco-israelita desencadearam uma perda de

confiança internacional, fuga de capitais e forte pressão sobre as reservas em

dólares do Banco de Inglaterra.

Surge, então, uma crise cambial, sob

forte chantagem financeira americana. Para defender a paridade, o Reino Unido “queimou”

reservas em dólares e recorreu ao FMI; ao mesmo tempo, os EUA deixaram claro

que não forneciam apoio financeiro enquanto Londres não recuasse militarmente. Perante

a ameaça de colapso da libra e racionamento de petróleo (pagável em dólares), o

governo britânico ordenou o cessar-fogo e a retirada – a famosa “humilhação de

Suez”.

Qual foi,

então, o efeito na libra e no estatuto britânico? A crise acelerou a percepção de que a libra já não

podia funcionar como moeda âncora global sem Washington; a sua credibilidade

como reserva foi corroída e seguir‑se‑iam novas crises e a desvalorização de

1967. Politicamente, Suez cristalizou o fim de facto da pretensão britânica a

grande potência independente e marcou a transição para um papel subordinado ao

eixo dólar/EUA. Em resumo: Suez não “matou” a libra, mas expôs brutalmente um

declínio já em curso e mostrou que a chave do sistema monetário e energético

passara para os EUA.

Podemos estabelecer paralelos com a

crise actual do dólar e dos EUA? Hoje,

fala-se de “crise do dólar” ou “desdolarização” devido a três factores

principais: o uso de sanções financeiras, o aumento da dívida e os avanços

tecnológicos que facilitam alternativas.

No que concerne

às sanções e procura de alternativas, o uso

intensivo de sanções (Irão, Rússia, etc.) através do controlo do sistema

dólar/Swift incentiva países como China, Rússia e membros dos BRICS a criar

mecanismos paralelos, aumentar o uso do yuan, rublos ou moedas locais e

discutir moedas de reserva alternativas. Tal como o Egipto usou a

nacionalização de Suez para desafiar o controlo anglo-francês do canal, alguns

estados hoje usam acordos energéticos em yuan ou moedas locais para desafiar o

“canal” financeiro dominado pelo dólar.

Em relação à dívida,

à política interna e à confiança, investigadores

e o próprio FMI notam que a participação do dólar nas reservas globais caiu

progressivamente (ainda acima de 55–60%, mas em queda gradual), enquanto a

dívida pública e a polarização política americana levantam dúvidas sobre a

qualidade da governação. Tal como a fragilidade económica britânica pós-guerra

condicionou Suez, a trajectória da dívida e as crises internas nos EUA podem, a

prazo, afectar a confiança no dólar como activo absolutamente “sem risco”.

No que diz

respeito à tecnologia e pluralização de meios de pagamento, os sistemas de pagamentos alternativos, moedas digitais de

bancos centrais (como o e-CNY chinês) e fintechs reduzem custos de

transaccionar noutras moedas, o que torna menos “obrigatório” passar pelo dólar

em algumas cadeias de valor.

Mas há diferenças

estruturais importantes. Os

paralelismos são úteis, mas as diferenças são fundamentais. Em primeiro lugar, a

posição de partida. Isto é, o Reino Unido, em 1956, apresentava uma economia

esgotada pela guerra, um império em desintegração, com a libra já em declínio

desde 1914 e fortemente dependente de dólares. Por outro lado, os EUA hoje

continuam a ser a maior, ou a segunda maior, economia, o maior mercado

financeiro integrado, com Treasuries ainda vistos como o principal activo

“porto seguro”. Depois temos a escala da moeda de reserva. Assim, a liberdade

da libra já era partilhada com o dólar desde Bretton Woods e entrou em declínio

irreversível nos anos 50-60. O dólar, por seu turno, ainda representa a maior

fatia das reservas, da facturação do comércio internacional e da dívida

externa, apesar da erosão gradual. Temos ainda os rivais sistémicos, ou seja, nos

anos 50, o substituto natural da libra era o dólar americano, apoiado no PIB,

no ouro e no poder militar. Ao contrário, hoje não existe um (único) substituto

claro do dólar: o euro, o yuan, o ouro, as moedas regionais e, possivelmente,

os activos digitais concorrem (mesmo) entre si.

Que

paralelismo é razoável, então, fazer? Um paralelismo forte: em ambos os casos, Suez

e Irão, o poder geopolítico e o estatuto monetário estão ligados. Suez mostrou

que quem controla o financiamento e a moeda de reserva também controla o limite

da aventura militar alheia: os EUA forçaram Londres a recuar ao estrangular a

libra. Hoje em dia, rivais dos EUA tentam reduzir a capacidade de Washington de

usar o dólar como arma (sanções, congelamento de reservas), promovendo a “desdolarização”

para ganhar margem estratégica.

Assinale-se,

ainda, um paralelismo mais fraco, porém pertinente. Tal como Suez marcou um “ponto

de inflexão simbólico” no declínio britânico, sucessivas crises (guerra no

Iraque, crise financeira de 2008, polarização interna, uso extensivo de

sanções) podem ser vistas como passos na erosão relativa do poder dos EUA –

inclusive do privilégio exorbitante do dólar.

Mas há uma diferença decisiva. 1956 foi

um choque quase terminal para a libra; o processo actual do dólar é lento,

parcial e ainda sem um substituto claro. Em vez de um “momento Suez” único, o

dólar enfrenta uma “longa erosão” num mundo multipolar, em que a pergunta não é

“que moeda substitui o dólar?”, mas “até que ponto o dólar será apenas o maior

entre vários polos monetários?” Alguns analistas olham para o dólar e veem “um

novo 1956” (Suez/libra), outros veem um “império cansado, mas ainda sem rival”.

A diferença vem, sobretudo, de que os dados privilegiam (dívida, sanções, BRICS

vs. redes financeiras, ausência de alternativa) e de como interpretam os precedentes

históricos.

Porque é que se fala então em

declínio irreversível do dólar? Em

primeiro lugar, façamos um paralelo histórico entre libra e dólar. Há

toda uma literatura “doomista” (catastrofista, negativa) a argumentar que o

dólar está a repetir o padrão da libra: excesso de dívida pública, impressão de

moeda muito acima do crescimento real, erosão de confiança externa e, mais

tarde, uma crise de confiança súbita. Alguns chegam a propor datas (2027, etc.)

com base em analogias com ciclos de 70–90 anos das moedas de reserva e na

trajectória de endividamento e “financialização” pós-2008.

Que dados se podem apontar para a

desdolarização e reserva? A

participação do dólar nas reservas cambiais caiu de cerca de 90% em 1960 para

~45% em 2023, com aumento de ouro, renminbi, dólar canadiano e outras moedas

nas carteiras de bancos centrais. Em dívidas e obrigações internacionais, a

quota do dólar também desceu (por exemplo, na dívida obrigacionista de ~50%

para ~30%). No comércio de energia, uma fatia “grande e crescente” de contratos

de petróleo e gás já é liquidada em moedas não-dólar, sobretudo em acordos

Rússia–China–Índia–Brasil, o que reduz a necessidade de reservas em USD e em Treasuries.

Na “arma” financeira e na reacção

política, o uso extensivo de sanções

financeiras e do controlo do sistema SWIFT contra cerca de um quarto dos países

(Rússia, Irão, Venezuela, etc.) é visto como um incentivo directo a

arquitecturas alternativas de pagamento e de reservas. Os BRICS e outros fóruns

do Sul Global trabalham precisamente nessa direcção, procurando pagar energia e

matérias-primas em moedas locais ou em yuan, para reduzir exposição ao dólar e

à jurisdição americana.

Depois, temos a dívida e a

fragilidade internas dos EUA, onde surgem analistas críticos que sublinham o nível de dívida americana (mais de 100% do PIB), a

necessidade de refinanciar grandes volumes de Treasuries a taxas mais altas e a

polarização política que já levou a downgrades de rating e a repetidos impasses

sobre o “debt ceiling”. A tese é: tal como o Reino Unido pós-guerra, os EUA

estão a corroer o activo-chave da moeda de reserva – a confiança na solidez

fiscal e institucional – e, quando os detentores estrangeiros “acordarem”, a

saída pode ser rápida, como no caso da libra.

Daqui vem a leitura “irreversível”: o

processo já começou (queda de quota nas reservas, uso abusivo de sanções,

dívidas crescentes) e, tal como com a libra, só falta o “momento Suez” que

torna visível o que já estava estruturalmente decidido.

Será que há uma resiliência

prolongada? Há uma rede, existe inércia

e ausência de alternativa única. Estudos de bancos centrais e de casas

como J.P. Morgan ou GS sublinham que, apesar da diversificação, o dólar

continua dominante em FX (c. 88% das transacções), trade invoicing (c. 40%),

passivos transfronteiriços (c. 50%) e dívida em moeda estrangeira (c. 70%).

Detectamos também um poderoso efeito de

rede: uma vez instalada, uma moeda dominante é difícil de substituir porque

todas as empresas, bancos e sistemas de pagamento estão calibrados para ela;

mudar implica custos massivos de coordenação, o que cria “histerese”

(resistência à mudança) a favor do dólar.

Depois existe a profundidade dos

mercados e o estatuto de porto seguro. Nenhum

outro país oferece algo comparável à profundidade, liquidez e transparência do

mercado de Treasuries e de derivados em dólares, que é a âncora de colateral e

de funding do sistema financeiro global.

Em momentos de stress (crises

financeiras, guerras), os fluxos continuam a correr para activos em dólares –

mesmo quando a narrativa mediática fala de “fim do dólar” –, o que mostra que,

na prática, os agentes ainda o veem como um porto seguro de último recurso.

Não esqueçamos o peso das instituições

e do Estado de direito. Argumentos pró-resiliência

insistem que os EUA ainda têm um sistema jurídico previsível, bancos centrais

independentes, tribunais relativamente estáveis e capacidade de emitir moeda de

reserva com credibilidade – algo que nem a China (por falta de liberalização de

capitais) nem a zona euro (por incompletude política) oferecem plenamente. Mesmo

defensores de “desdolarização” reconhecem que esta tende mais a significar diversificação

gradual do que substituição pura e simples do dólar por outra moeda.

Podemos fazer outra leitura: “novo

plateau, não colapso”. Análises mais

equilibradas falam de um “recuo de nível”: o dólar perde peso relativo

(sobretudo em reservas oficiais e energia), mas estabiliza num patamar ainda

muito superior ao de qualquer rival, funcionando como “âncora de emergência”

por décadas. A tese aqui é que estamos a passar de uma hegemonia quase absoluta

para um sistema mais fragmentado, com o dólar ainda no topo, mas rodeado de

alternativas regionais (euro, yuan, moedas de grandes emergentes) – erosão

estrutural, não colapso súbito.

Em síntese: duas leituras do mesmo

processo

Ambos estão a descrever o mesmo fenómeno

– desdolarização como tendência real –, mas divergem na velocidade, na

irreversibilidade e, sobretudo, na probabilidade de um “momento Suez” abrupto

versus uma longa transição para um sistema monetário mais multipolar.

When mathematics

becomes irreversible, and history shines…

Why do empires not

fall due to wars?

The

Suez Crisis of 1956 was a key moment when it became obvious to London and the

world that British imperial power and the centrality of the pound could no

longer survive without Washington's financial and political endorsement.

Parallels with the current situation of the dollar and the US exist

(geopolitical pressure, high debt, contestation from rivals). Still, the

starting point is very different: in 1956, the United Kingdom was already in

structural decline, while the US remains by far the largest economy and the

main issuer of safe assets, even amid “de-dollarization” pressures.

The

Suez Crisis marked the beginning of the pound's collapse and the United

Kingdom's decline. First and foremost, it signals a clear dependence on the

dollar and the pound's vulnerability. After the Second World War, the pound

maintained a role as a reserve currency for the "land area," but it

was supported by American support lines and the Bretton Woods system (fixed

parity of US$2.80/GBP). The nationalization of the Suez Canal by Egyptian

President Nasser (1918-1970, president 1954-1970) in July 1956, and the

Anglo-French-Israeli military intervention triggered a loss of international

confidence, capital flight, and strong pressure on the Bank of England's dollar

reserves.

A

currency crisis then emerged, under strong American financial blackmail. To

defend the parity, the United Kingdom "burned" its dollar reserves

and sought assistance from the IMF; at the same time, the US made it clear that

it would not provide financial support until London withdrew militarily. Faced

with the threat of the pound collapsing and oil rationing (payable in dollars),

the British government ordered a ceasefire and withdrawal – the famous “Suez

humiliation.”

What,

then, was the effect on the pound and British status? The crisis

accelerated the perception that the pound could no longer function as a global

anchor currency without Washington; its credibility as a reserve currency was

eroded, and further crises and the devaluation of 1967 followed. Politically,

Suez crystallized the de facto end of Britain's claim to be a great independent

power. It marked the transition to a role subordinate to the dollar/US axis. In

short, Suez did not “kill” the pound, but brutally exposed a decline already

underway and showed that the key to the monetary and energy system had passed

to the US.

Can

we draw parallels with the current crisis of the dollar and the US? Today, there is

talk of a “dollar crisis” or “de-dollarization” due to three main factors: the

use of financial sanctions, increased debt, and technological advances that

facilitate alternatives.

Regarding

sanctions and the search for alternatives, the intensive use of sanctions

(Iran, Russia, etc.) through control of the dollar/Swift system encourages

countries like China, Russia, and BRICS members to create parallel mechanisms,

increase the use of the yuan, rubles, or local currencies, and discuss

alternative reserve currencies. Just as Egypt used the nationalization of the

Suez Canal to challenge Anglo-French control of the canal, some states today

use energy agreements denominated in yuan or local currencies to challenge the

dollar-dominated financial “channel.”

Regarding

debt, domestic politics, and confidence, researchers and the IMF itself note

that the dollar's share of global reserves has gradually declined (still above

55–60% but declining). In contrast, American public debt and political

polarization raise doubts about the quality of governance. How post-war British

economic fragility conditioned Suez, the debt trajectory, and internal crises

in the US may, in the long term, affect confidence in the dollar as an

absolutely “risk-free” asset.

Regarding

technology and the proliferation of payment methods, alternative payment

systems, central bank digital currencies (such as the Chinese e-CNY), and

fintechs reduce the costs of transacting in other currencies, making it less

“mandatory” to use the dollar in some value chains.

There

are important structural differences. Parallels are useful, but differences are

fundamental. First, the starting position. That is, the United Kingdom in 1956

had an economy exhausted by the war, a disintegrating empire, with the pound

already in decline since 1914 and heavily dependent on the dollar. On the other

hand, the US today continues to be the largest, or second-largest, economy and

the largest integrated financial market, with Treasuries still seen as the main

“haven” asset. Then we have the reserve currency's scale. Thus, the pound's

freedom had already been shared with the dollar since Bretton Woods, and the

pound entered an irreversible decline in the 1950s and 60s. The dollar, in

turn, still represents the largest share of reserves, international trade

revenue, and external debt, despite its gradual erosion. We also have systemic

rivals, that is, in the 1950s, the natural substitute for the pound was the US

dollar, backed by GDP, gold, and military power. In contrast, today there is no

(single) clear substitute for the dollar: the euro, the yuan, gold, regional

currencies, and possibly digital assets compete (even) with each other.

What

parallel is reasonable to draw, then? A strong parallel: in both cases, Suez

and Iran, geopolitical power and monetary status are linked. Suez showed that

whoever controls the financing and the reserve currency also controls the limit

of the other's military adventure: the US forced London to back down by

strangling the pound. Nowadays, US rivals are trying to reduce Washington's

ability to use the dollar as a weapon (sanctions, freezing of reserves),

promoting "de-dollarization" to gain strategic leeway.

It

should also be noted that there is a weaker, but pertinent, parallel. Just as

Suez marked a “symbolic turning point” in the British decline, successive

crises (the Iraq war, the 2008 financial crisis, internal polarization,

extensive use of sanctions) can be seen as steps in the relative erosion of US

power – including the exorbitant privilege of the dollar.

But

there is a crucial difference. 1956 was a near-terminal shock for the pound;

the current process for the dollar is slow, partial, and still without a clear

replacement. Instead of a single “Suez moment,” the dollar faces a “long

erosion” in a multipolar world, where the question is not “what currency

replaces the dollar?”, but “to what extent will the dollar be just the largest

among several monetary poles?” Some analysts look at the dollar and see “a new

1956” (Suez/pound), others see a “tired empire, but still without rival.” The

difference comes, above all, from the data they privilege (debt, sanctions,

BRICS vs. financial networks, lack of alternative) and how they interpret

historical precedents. Why, then, is there talk of an irreversible decline in

the dollar? First, let's draw a historical parallel between the pound and the

dollar. There is a whole "doomist" (catastrophist, negative)

literature arguing that the dollar is repeating the pound's pattern: excess

public debt, money printing far above real growth, erosion of external

confidence, and, later, a crisis of confidence. Some even propose dates (2027,

etc.) based on analogies with 70-90 year cycles of reserve currencies and the

trajectory of indebtedness and "financialization" post-2008.

What

data can be pointed to for de-dollarization and reserves? The dollar's share

of foreign exchange reserves fell from about 90% in 1960 to ~45% in 2023, as

the share of gold, renminbi, Canadian dollar, and other currencies in central

bank portfolios increased. In international debt and bonds, the dollar's share

also fell (for example, in bond debt from ~50% to ~30%). In energy trade, a

"large and growing" share of oil and gas contracts is already settled

in non-dollar currencies, especially in Russia-China-India-Brazil agreements, thereby

reducing the need for USD and Treasury reserves.

In

the financial "weapon" and political reaction, the extensive use of

financial sanctions and control of the SWIFT system against about a quarter of

countries (Russia, Iran, Venezuela, etc.) is seen as a direct incentive for

alternative payment and reserve architectures. The BRICS and other forums of

the Global South are working precisely in this direction, seeking to pay for

energy and raw materials in local currencies or in yuan, to reduce exposure to

the dollar and American jurisdiction.

Then,

we have the internal debt and fragility of the US, where critical analysts

highlight the level of American debt (more than 100% of GDP), the need to

refinance large volumes of Treasuries at higher rates, and the political

polarization that has already led to rating downgrades and repeated impasses

over the "debt ceiling." The thesis is: just like post-war Britain,

the US is eroding the key asset of the reserve currency – confidence in fiscal

and institutional soundness – and, when foreign holders "wake up,"

the exit could be quick, as in the case of the pound.

Hence

the "irreversible" interpretation: the process has already begun

(falling reserve quotas, abusive use of sanctions, growing debts) and, just as

with the pound, all that's missing is the "Suez moment" that makes

visible what was already structurally decided.

Is

there prolonged resilience?

1.

Network, Inertia, and the Absence of a Single Alternative

Studies

by central banks and firms such as J.P. Morgan and GS emphasize that, despite

diversification, the dollar remains dominant in FX (approx. 88% of

transactions), commercial invoicing (approx. 40%), cross-border liabilities

(approx. 50%), and foreign-currency debt (approx. 70%).

There

is a powerful network effect: once established, a dominant currency is

difficult to replace because all companies, banks, and payment systems are

calibrated to it; changing implies massive coordination costs, which creates

"hysteresis" (resistance to change) in favor of the dollar.

2.

Profund market depth and safe-haven status

No

other country offers anything comparable to the depth, liquidity, and

transparency of the Treasury and dollar derivatives market, which is the

collateral and funding anchor of the global financial system.

In

times of stress (financial crises, wars), flows continue to run to dollar

assets – even when the media narrative speaks of the “end of the dollar” –

which shows that, in practice, agents still see it as a haven of last resort.

3.

Institutions and the Rule of Law

Pro-resilience

arguments insist that the US still has a predictable legal system, independent

central banks, relatively stable courts, and the ability to issue reserve

currency with credibility – something that neither China (due to a lack of

capital liberalization) nor the eurozone (due to political incompleteness)

fully offers.

Even

proponents of “de-dollarization” acknowledge that it typically entails gradual

diversification rather than a simple replacement of the dollar with another

currency.

4.

Reading “new plateau, not collapse.”

More

balanced analyses speak of a “level retreat”: the dollar loses relative weight

(especially in official reserves and energy). However, it stabilizes at a level

far superior to any rival's, serving as an “emergency anchor” for decades.

The

thesis here is that we are moving from an almost absolute hegemony to a more

fragmented system, with the dollar still at the top, but surrounded by regional

alternatives (euro, yuan, currencies of major emerging markets) – structural

erosion, not sudden collapse.

Two

readings of the same process

•

“Suez/pound field”: looks at the debt, sanctions, and loss of participation in

reserves, and concludes that the trajectory is one of irreversible decline,

only masked by inertia – today we would be in an American “1956”, waiting for

the shock that formalizes the loss of hegemony.

•

“Resilience field”: looks at data on the effective use of the dollar in FX,

trade, and debt, and at the coordination costs of changing the standard, and

sees a still robust hegemony, to be slowly diluted by diversification, but

without a clear candidate for total replacement in the foreseeable horizon.

Both describe

the same phenomenon – de-dollarization as a real trend – but they diverge in

speed, irreversibility, and, above all, in the probability of an abrupt “Suez

moment” versus a long transition to a more multipolar monetary system.

COMENTÁRIOS

Historiador, professor, investigador e autor, além de consultor e colaborador em publicações periódicas regulares.